Better Together: How Leverage Can Enhance CRE Returns

Leverage plays a central role in commercial real estate investing, making it essential for investors to understand both its benefits and drawbacks. At its core, leverage is the use of borrowed capital to acquire or control an asset. When applied thoughtfully, leverage can enhance returns, improve capital efficiency, and support long-term portfolio growth. When applied without discipline, it can introduce additional risk.

At a basic level, leverage allows investors to control a larger asset with less equity. By combining investor capital with debt, the same property can be acquired with a smaller upfront equity investment while still benefiting from the full income and appreciation of the asset.

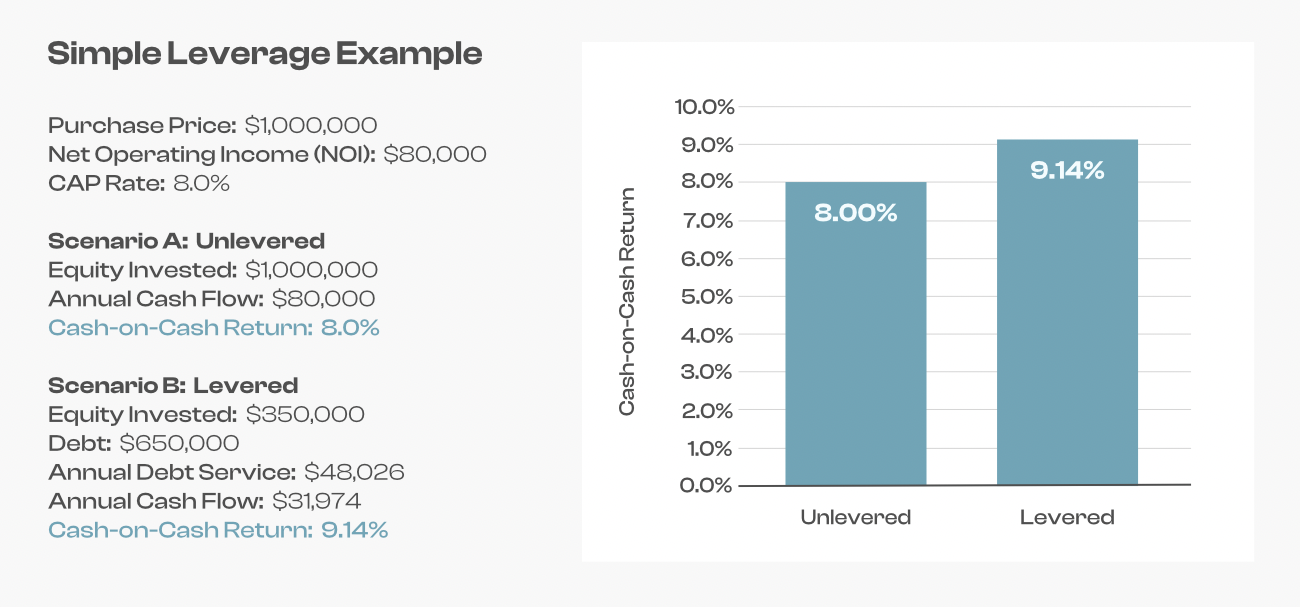

When a property generates stable cash flow, leverage can meaningfully improve equity-level returns. With less equity invested, the same net operating income may translate into higher cash-on-cash returns, stronger equity multiples, and improved internal rates of return over time.

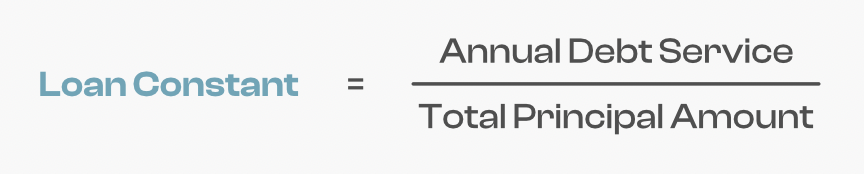

In general, leverage enhances returns when an investment’s cap rate exceeds the debt’s loan constant. The loan constant represents annual debt service as a percentage of the total loan balance. When this relationship is true, leverage can positively impact equity returns compared to an all-cash investment. The simple example below illustrates an unlevered versus levered acquisition purchased at a cap rate above the loan constant. It is important to note that changes in income, interest rates, or property value can alter this outcome, which is why complete underwriting and market analysis should be performed for every deal.

Beyond return enhancement, leverage can provide investors with greater flexibility and scale. By reducing the amount of equity required per investment, leverage allows capital to be deployed across multiple assets rather than concentrated in a single deal. This can improve diversification by spreading exposure across different tenants, markets, and lease structures.

Leverage can also enable participation in larger, higher-quality assets that may otherwise require significant all-cash commitments. When used prudently, this can improve portfolio quality while maintaining appropriate risk controls.

Within industrial real estate, the effects of leverage can often be more predictable due to longer lease terms, mission-critical assets, and simpler operating expense structures. Properties leased under NNN or absolute-net structures, in particular, tend to produce more stable cash flow, which supports the responsible use of debt.

While leverage can enhance returns, it also introduces fixed obligations. Debt service must be paid regardless of occupancy or market conditions. As leverage increases, so does sensitivity to changes in cash flow, interest rates, and lease rollover. For this reason, leverage should never be evaluated in isolation. It must be considered alongside asset quality, tenant strength, lease structure, and overall market conditions. From an investor’s perspective, leverage works best when it supports the business plan rather than drives it. The objective is not to maximize debt, but to use it in a way that enhances return potential while maintaining flexibility and downside protection. Conservative underwriting and appropriate margins for unexpected changes in cash flow remain critical.

At Legacy West Partners, leverage is viewed as a supporting tool, not a substitute for strong fundamentals. Our focus remains on acquiring well-located industrial assets, maintaining durable cash flow, and structuring capital in a way that supports long-term performance across market cycles. Used thoughtfully, leverage can enhance returns and improve capital efficiency. Used without discipline, it can quickly work against the investor.

Disclosures

This material is for informational purposes only and does not constitute investment, legal, or tax advice. Nothing herein should be construed as a recommendation or solicitation to buy or sell any security or investment. Any investment involves risk, including the possible loss of principal. Readers should consult their own advisors before making investment decisions.